What’s the Difference Between Bonding and Insurance?

Is there really a difference between surety bonds and insurance? It’s easy to get confused when the terms “surety bond,” “surety bond insurance,” and “surety insurance” are used interchangeably.

In short, no — bonds are not the same as insurance.

Surety bonds actually function as a line of credit between the surety and the bonded principal. This reassures the party requiring the bond that the principal will meet their contractual obligations.

Comparing Bonds vs Insurance

Being bonded protects consumers from improper business conduct while being insured protects a business by transferring financial risk to an insurance company.

Explore the key differences between being bonded vs being insured in the table below:

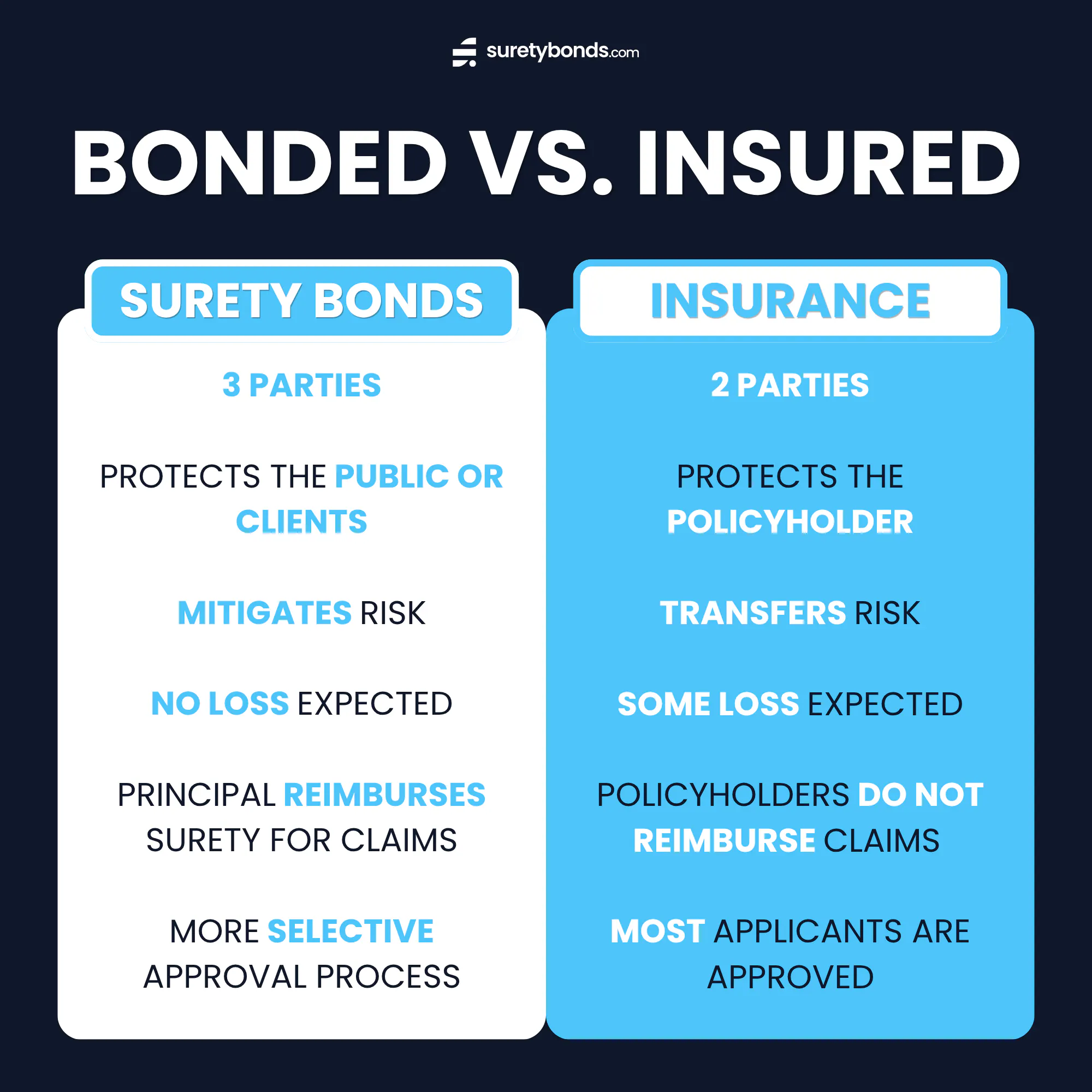

| Surety Bond | Insurance Policy |

|---|---|

| 3 Parties: Principal, Obligee, Surety Provider | 2 Parties: Policyholder, Insurance Provider |

| Protects the public | Protects the policyholder |

| Acts as a risk-mitigation contract | Acts as a risk-transfer tool |

| Loss is not expected by the provider | Loss is factored into pricing |

| Principal is responsible for refunding the surety for claims | Policyholders are not liable for repaying claims |

| Sureties take selective risks when underwriting | Insurers write most risks and aim to qualify every applicant |

Who’s Protected in a Surety Bond vs Insurance Policy?

In a general liability insurance policy, the insured business is covered for basic claims such as property damage, accidents and injuries

A surety bond contract does not protect the business but rather covers the obligee or the business’ customers from financial loss.

Here’s a quick review of how the three-party bond contract works:

How Do Premiums Work for Bonds vs Insurance?

Insurance premiums cover potential business losses while surety bond premiums act as a line of credit to ensure a principal fulfills the bond obligations.

- Insurance: Monthly premium funds from many policyholders are pooled to cover future claims.

- Surety Bonds: Individual applicants pay an upfront premium to cover underwriting costs and assumption of risk by the surety. Bond premiums do not cover future claims.

Do You Pay Surety Bonds Monthly?

No. Unlike monthly insurance premiums, surety bonds are a single, upfront purchase — typically for a one-year term.

How Are Claims Handled for Bonds vs Insurance?

Bonds and insurance both involve claims payments when things go wrong. But here’s how they differ:

- Insurance claims: The insurance provider is liable for paying claims using pooled premium funds.

- Surety bond claims: The bonded principal is liable for reimbursing the surety for claims payments.

With most surety bonds, the principal will sign an official indemnity agreement that stipulates they will repay the surety for any claims.

Why You Should Avoid Surety Bond Claims

While insurance claims are often out of one’s control, you should avoid surety bond claims at all costs.

If you have a $25,000 bond and a customer files a valid $3,000 claim, you’ll need to reimburse the surety for the $3,000 payment. Many insurance providers will also cancel the bond mid-term if a claim is made to avoid future losses.

How to Get Bonded and Insured Now

SuretyBonds.com can issue your surety bond in as little as two minutes. Buy your bond online instantly or apply for a free quote now.

Start by selecting your state below to find the bond you need: